The Great Era of Entrepreneurship

The post-industrial contract between corporate employers and salaried knowledge workers is undergoing a phase of structural dissolution. For much of the twentieth century, the dominant model of socioeconomic advancement was the “career”: a linear progression through hierarchical organizations that promised long-term security in exchange for time discipline, cognitive labor, and institutional loyalty.

That model no longer holds.

In the current macroeconomic environment, the traditional career has shifted from a pathway to stability into a constrained, risk-exposed cash-flow arrangement. This shift is driven by compounding forces: rising inequality, financialization of corporate governance, algorithmic gatekeeping in hiring and promotion, and the rapid emergence of generative AI systems that are reshaping the structure of knowledge work itself.

As a result, the corporate job is increasingly better understood not as an endpoint, but as a financing mechanism.

A growing number of knowledge workers are responding to this shift by reinterpreting salaried employment as a source of non-dilutive capital used to fund independent economic activity. Under this framing, the employer provides stable cash flow, while the worker allocates surplus time and cognitive capacity toward the construction of privately owned digital assets.

Macroeconomic Context

The structural migration of elite talent away from traditional corporate pipelines is driven by the convergence of two strong macroeconomic forces: the exponential escalation of living costs due to pervasive rent-seeking across the economy, and the systemic erosion of “safe” institutional, familial, and political systems. Together, these forces exert persistent upward pressure on basic survival costs while simultaneously undermining long-term professional and financial predictability, compelling rational economic agents to hedge across every dimension of their lives.

The first force, the rising inequality driven by rent-seeking, manifests most clearly in the decoupling of median wages from the cost of wealth-generating assets, particularly residential real estate. For most of the 20th century, the ratio between median household income and median home prices in the United States remained relatively stable, with home prices fluctuating between roughly 3.0 and 3.4 times annual median household income: this stability allowed salaried employees to reliably convert labor income into real estate equity, enabling long-term wealth accumulation and participation in the middle class. However, in the early 21st century, home price growth began to significantly outpace real income growth. By 2024, the national median single-family home price had risen to approximately 5.0 times median household income, matching the historic highs seen during the mid-2000s housing bubble. In high-productivity metropolitan areas—where premium white-collar employment is concentrated—this ratio has reached even more extreme levels, rendering homeownership mathematically inaccessible for many salaried workers.

A similar pattern is observable across much of the world.

This appreciation is largely attributed to rent-seeking dynamics across the economy, including restrictive municipal zoning regimes, institutional acquisition of single-family housing stock, and broader supply constraints. While median home prices in major markets increased by approximately 24% to 79% between 2019 and 2024, median incomes in those same regions rose only about 8% to 36%. As a result, the geography of corporate capitalism has become economically constraining: roughly 50% of renters in the United States now spend at least 30% of their income on rent, while approximately 25% allocate over 50%, leaving minimal capacity for savings or capital accumulation. Empirical research further suggests that elevated rent burdens correlate with increased precarity and homelessness; for instance, a $100 increase in median rent has been associated with a 9% rise in local homelessness rates.

This structural barrier to asset ownership has weakened the psychological foundations of the traditional corporate career model: when a standard salaried role no longer reliably enables homeownership, family formation, or wealth accumulation, the implicit exchange of “time for stability” becomes increasingly untenable. Younger cohorts, and particularly Gen Z and Millennials, recognize this shift and increasingly decouple personal identity from employer affiliation, especially as many corporate roles are perceived as temporary arrangements with limited long-term security. This structural recalibration is reflected in global survey data: in the Deloitte Global Gen Z and Millennial Survey, 69% of Gen Z and 64% of Millennials report that housing affordability directly influences their career decisions and geographic mobility, while over 55% have delayed major life milestones such as homeownership or family formation due to financial constraints.

As the single corporate salary has been progressively stripped of its capacity to provide long-term security, income diversification has shifted from a discretionary strategy to a structural necessity. Today, 64% of Gen Z view multiple income streams as essential to navigating the modern economy, a dynamic that has contributed to the rise of the “side hustle” generation. Surveys indicate that nearly two-thirds of individuals aged 18 to 35 have either started or intend to start a private venture, with 65% actively engaging in entrepreneurial activity.

The primary motivations behind this shift are not transient trends but structural responses to economic conditions, chiefly a pursuit of autonomy (49% citing a desire to be their own boss) and financial sovereignty in a system where the traditional corporate career ladder has largely stalled.

I: The History of Work

To fully comprehend the rise of the solopreneur and the strategic reallocation of labor in the modern digital economy, one must analyze the history of work over the long-term. The modern idea of a “career”, defined as a lifelong, structured path of advancement through large bureaucratic organizations and institutions, is not the default state of human economic activity. Rather, it is an historically brief, highly anomalous development of the 19th and 20th centuries, forged during the Industrial Revolution and the subsequent rise of corporate capitalism. Prior to industrialization, the vast majority of human labor was decentralized, task-oriented, and functionally self-employed: in agrarian societies, local communities, and craft guilds, workers possessed direct ownership of their tools, their workshops, and the physical output of their labor. In other words, we could say the pre-industrial economy largely operated as a localized gig economy. Manufacturing workers, such as spinners, weavers, and smiths, were not compensated for their time, but were rather paid task-rates or piece-rates for their specific output. Furthermore, work patterns were deeply precarious and characterized by extreme seasonal variations.

Historical analyses of actual pre-industrial workplaces demonstrate that the concept of a steady, year-round, forty-hour-a-week job did not exist. During the dark winter months of January and February, construction, shipping, and agricultural activities slowed to a virtual halt due to light constraints and frozen transport routes. For example, during the rebuilding of St. Paul’s Cathedral in London between 1700 and 1710, a key mason contractor’s team worked 45% fewer days during the first quarter of the year compared to the summer months, while the cathedral’s general laborers saw their active working days cut in half in January compared to July. Workers moved constantly from site to site, and employers maintained zero long-term retention obligations, mimicking the zero-hours contracts of the modern gig economy.

The Industrial Revolution fundamentally disrupted this decentralized model of production. And gave birth to what we now know as capitalism.

The development of centralized, capital-intensive manufacturing technologies, such as coal-powered factories, steam engines, and synchronized assembly lines, required the physical consolidation of human labor. A single factory could not operate if individual spinners and weavers chose their own seasonal schedules or worked from remote cottage locations. Therefore, industrial capitalism had to systematically construct a new social class: the salaried wage-laborer. This transition required the imposition of strict, unnatural time discipline. Workers had to be socialized to sell their time rather than their output. Early industrialists, such as Richard Arkwright, designed factory systems that utilized fines, physical surveillance, and automated steam bells to enforce synchronized, rigid shifts. And to coordinate this massive mobilization of human labor, modern corporate bureaucracies emerged, creating intermediate managerial, clerical, and administrative roles.

This corporate apparatus promised a historic trade-off: in exchange for submitting to time-discipline, surrendering ownership of their intellectual property, and dedicating their sole professional loyalty to the firm, workers received a stable wage, shelter from macroeconomic volatility, and a predictable, lifelong career path. Ironically, if we described this modern concept of a “career”, meaning selling one’s cognitive autonomy to a single corporate entity for forty years in exchange for a leased salary, to a pre-industrial worker, they would likely assume we were talking about slavery or debt bondage: indeed, the early industrial labor market was often characterized by the “company store” or truck system, where monopolistic employers paid workers in private scrip redeemable only at overpriced, company-owned retail stores, keeping the workforce in a state of permanent debt-slavery. In many ways, the modern high-rent corporate city operates as a digital-era company store, where the high salaries paid to tech and finance workers are immediately clawed back by institutional landlords and urban service cartels, keeping the modern knowledge worker in a state of perpetual financial captivity.

As the digital economy matures, the physical and material foundations that supported the industrial corporate model are rapidly disintegrating. The widespread availability of low-cost computing, cloud distribution, and generative artificial intelligence has dramatically reduced the capital requirements for high-leverage production.

Consequently, the global labor market is undergoing a structural reversion to pre-industrial patterns of decentralized, output-based self-employment. The industrial era’s attempt to force the human agent into a rigid, lifetime corporate mold is ending. The modern knowledge worker is transitioning from a corporate captive back to an independent digital craftsman, utilizing the corporate job not as a final destination, but as a temporary mechanism to fund their private digital estate.

II: The Structural Breakdown of the Corporate Pipeline

The systemic retreat of elite talent away from the corporate ladder is accelerated by the profound structural decay of the corporate pipeline itself: modern corporate cultures have become increasingly bloated, bureaucratic, and dysfunctional, characterized by human resource departments unable to recognize raw talent, recruitment algorithms reducing human experience to rigid keyword matches, and DEI initiatives that reward superficial optics over objective competence. Under these conditions, capable, highly motivated individuals are finding that the corporate system no longer has room for them, forcing them to exit the traditional labor market to preserve their human capital.

The most glaring manifestation of this institutional decay is the collapse of traditional credentialism: for decades, prestigious white-collar credentials, most notably the MBA, served as the primary signaling mechanism, for entry into elite management, consulting, and financial pipelines. However, the economic value of these expensive, high-debt degrees has plummeted. Faced with a highly volatile job market and the rapid cognitive capabilities of generative AI, high-potential professionals are realizing that the traditional two-year MBA no longer provides an acceptable ROI; consequently, prestigious business schools are facing a historic application crisis, with many programs forced to offer deep tuition discounts of up to 50% to fill their classes as overall application volumes collapse.

Indeed, according to admissions data from the 2023–2025 cycle, full-time U.S. MBA programs have experienced steep, unprecedented declines in applications and international student enrollment. Historically, graduate management education has behaved in a strictly counter-cyclical fashion: during periods of economic downturn or white-collar layoffs, professionals routinely left the workforce to seek shelter in business schools. But this time is different, signaling a structural and permanent devaluation of white-collar credentials in the digital market era: high-potential candidates are increasingly uncertain not only about the short-term job market, but also about the long-term, structural value of traditional management training altogether.

But it makes sense: the CV itself has become an obsolete relic. Optimized for a physical world characterized by opaque expertise, the résumé was designed to prove competence through third-party institutional gatekeepers (ie. prestigious university brand names, elite employer stamps, and physical pieces of paper). In the digital era, however, the internet has made human cognitive traits visible at scale for the first time. And once baseline technical skills are met, what actually matters in a high-velocity economy is independent judgement, adaptability, communication, taste and the capacity to solve nove problems.

A traditional CV is a terrible proxy for these dynamic traits, as it merely tells an employer where someone sat and studied. Conversely, a digital footprint, such as a public social media profile, a personal newsletter, or an open-source code repository, provides an infinitely more informative proof of competence: this really demonstrates how an individual thinks, how they communicate, what they are curious about, who respects their ideas, and whether they can consistently produce valuable concepts in public.

As traditional corporate screening algorithms lock out non-standard talent, the public digital footprint has emerged as a decentralized authority engine, landing high-leverage opportunities and partnerships entirely independent of institutional credentials.

III: Economic Modeling of Corporate Incentives

The structural dysfunction of modern corporate employment is ultimately a crisis of incentive design.

In any highly structured bureaucratic organization, the compensation architecture is fundamentally decoupled from individual productive output. Indeed, employees are paid primarily for their input, meaning the number of hours they remain logged into corporate systems or physically seated at their desks. However, this decoupling of compensation from output creates a highly perverse economic incentive: cbecause uncompensated overperformance carries zero marginal financial upside while introducing significant cognitive exhaustion and layoff risk, the rational incentive for any corporate employee is to do as little as possible while making sure they do not get fired.

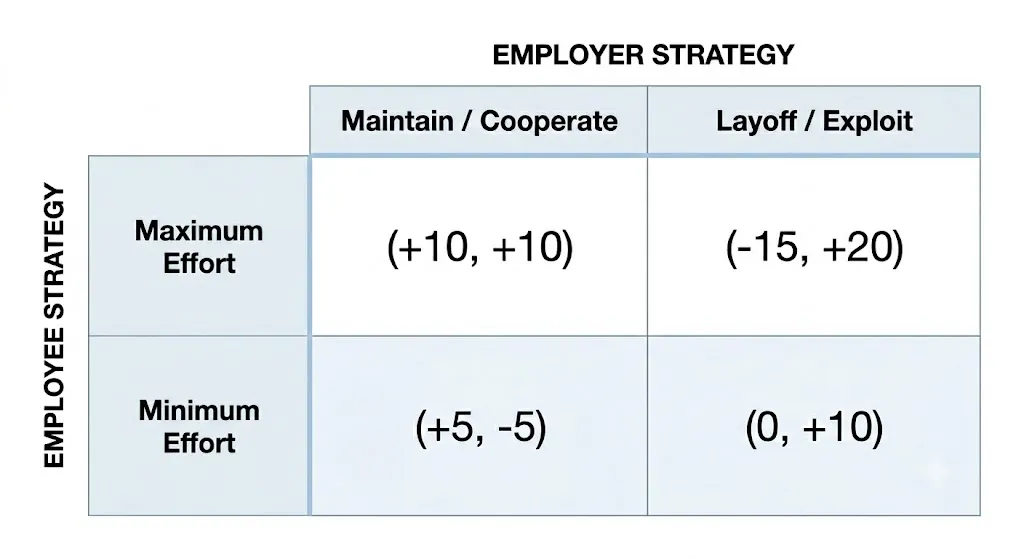

This behavior can be analyzed using the game-theoretic framework of the Minimum Effort Game.

In this coordination game, a corporate team or department represents a group of players who must decide how much effort to allocate to a project, where effort levels are bounded between a minimum level () and a maximum level (). Each unit of effort allocated by an individual carries a linear personal cost .

Crucially, the collective performance bonus or payoff of the group is determined strictly by the minimum effort level chosen by any single member of the team, multiplied by a scaling factor . The payoff function for any individual player is modeled as:

Under this mathematical payoff structure, coordinating on the maximum effort level ( for all players) represents the payoff-dominant Nash equilibrium, yielding a net payoff of:

However, this equilibrium is highly unstable and carries immense payoff risk. If an overachieving employee decides to dedicate maximum effort (), but a single disengaged teammate decides to coordinate on the minimum effort level (, “quiet quitting”), the group’s minimum effort collapses to 1. The overachieving employee’s final payoff becomes:

Conversely, the quiet quitter who allocated minimum effort () pays a personal cost of only , resulting in a positive payoff of:

In this game, overperformance in a group-coordinated corporate structure with a flat, non-equity bonus system is a highly irrational, wealth-destroying strategy. The moment a single employee detects or anticipates disengagement among their peers, their rational response is to immediately reduce their own effort level to protect themselves from a negative payoff. And this defensive reduction of effort cascades rapidly through the organization, driving the entire team to coordinate on the lowest stable effort level.

This mathematical reality is the economic foundation of “quiet quitting”: it is a rational, defensive coordination strategy designed to optimize personal utility under asymmetric information and misaligned corporate incentives.

This game-theoretic pattern is then further shaped by the relational climate of the workplace. In market pricing climates, where transactional, self-interested exchanges are the organizational default, quiet quitting is highly prevalent but accepted as a natural baseline behavior; however, in communal sharing climates, which emphasize reciprocity, mutual aid, and “corporate family” values, quiet quitting can trigger severe interpersonal friction: when an individual quiet quits in a harmonious climate, they shift the cognitive and operational burden onto their peers, who must exert uncompensated extra effort to maintain project standards. And while these peer groups may initially offer support, the persistence of quiet quitting eventually triggers intense resentment, social sanctions, and collective monitoring, as coworkers seek to protect themselves from uncompensated exploitation.

The only systemic solution to this incentive collapse is to abandon the industrial input-monitoring model: the absolute best way to improve organizational morale and productive output is to tie compensation, at least partially, to measurable output KPIs rather than hours worked. By paying for objective output rather than time spent, the firm aligns the employee’s financial interests with organizational productivity. Indeed, under an output-based compensation contract, an employee who completes their work faster is rewarded with temporal autonomy rather than a higher volume of busy work, completely eliminating the incentive to quiet quit and restoring productive agency to the worker.

IV: Bootstrapping on the Corporate Dime

The assumption that consistent corporate performance will be rewarded with long-term retention and predictable career advancement no longer reflects the realities of the modern labor market. In an economy defined by recurring layoffs, organizational restructuring, and increasingly transactional employment relationships, workers must rethink the role that salaried employment plays in their long-term economic strategy.

The alternative framework is straightforward: secure a traditional salaried position, but treat the resulting income not as an end in itself, but as a source of non-dilutive capital used to finance assets that you own.

This approach addresses the primary constraint faced by many aspiring entrepreneurs: the cost of survival during the construction phase. Bootstrapping a business from personal savings creates constant financial pressure, forcing founders to balance long-term value creation against the immediate need to preserve runway; VC solves the liquidity problem but introduces a different set of constraints, including equity dilution, governance oversight, and growth expectations that may not align with the founder’s objectives.

A salaried job occupies a unique middle ground.

The paycheck arrives on a predictable schedule: housing, food, healthcare, software, and other baseline expenses are covered by wage income rather than by the venture itself. As a result, the entrepreneur is able to experiment, iterate, and build over longer time horizons without placing their financial survival at immediate risk.

Viewed through a portfolio lens, an individual’s economic position can be modeled as a combination of wage income and entrepreneurial equity:

Where represents expected wage income, represents the probability of employment termination, and represents the value of the private venture as a function of time invested outside of work. The parameter captures the uncertain relationship between effort and entrepreneurial success.

In a highly volatile labor market where is elevated, relying solely on the corporate wage () is an unstable strategy which creates a highly concentrated risk profile: a single employer controls the overwhelming majority of the individual’s cash flow, making economic stability contingent on decisions over which the worker has little influence.

The objective is therefore not to abandon salaried employment immediately, but to use it strategically:

- The wage functions as a stabilizing asset.

- The venture functions as a source of ownership, optionality, and long-term upside.

- Employment provides the resources required to survive in the present; entrepreneurial activity creates the possibility of independence in the future.

The optimal portfolio strategy is to maintain as a continuous, baseline subsidy, treating the corporate time allocation as a fixed operational cost required to secure non-dilutive funding, while directing the entire cognitive and financial surplus toward building .

The resulting portfolio differs significantly from both traditional venture-backed entrepreneurship and pure bootstrapping.

| Strategic Dimension | Venture-Backed Startup | Personal Bootstrapping | Salary-Funded Venture |

|---|---|---|---|

| Equity Ownership | Reduced through repeated dilution | Full ownership retained | Full ownership retained |

| Strategic Control | Shared with investors and board members | Fully retained | Fully retained |

| Financial Runway | Limited by funding cycle | Limited by personal savings | Extended by ongoing wage income |

| Primary Risk | Investor expectations and growth requirements | Capital depletion | Employment disruption |

| Upside participation | Shared among stakeholders | Fully retained | Fully retained |

However, adopting this strategy also requires abandoning the notion that employment is a partnership between equals.

Indeed, the modern employment relationship is structurally asymmetric: employees exchange time, expertise and labor for compensation, while ownership of the resulting IP, strategic assets, and future cash flows remains with the firm. Workers participate in the current income, but they rarely participate meaningfully in the long-term appreciation of the assets they help create. Therefore, employment should be understood as a commercial relationship rather than a moral obligation. And as such, the rational agent must adopt an equally transactional framework: one owes no professional loyalty without equity.

For workers without equity, extraordinary effort generates disproportionate returns for the institution relative to the individual. The rational objective is therefore not to maximize attachment to the employer, but to maximize the conversion of wage income into assets that remain under personal ownership.

V: The Productivity Arbitrage

The widespread adoption of generative AI and the normalization of remote work have created a new form of economic opportunity: productivity arbitrage.

By leveraging tools such as ChatGPT, Claude, and Gemini, skilled knowledge workers can now automate or accelerate large portions of their daily workload. Tasks that once required a full workday can often be completed in a fraction of the time while meeting, or even exceeding, the quality standards expected by employers. Yet most organizations continue to evaluate labor through frameworks inherited from the industrial era: compensation remains tied to hours, availability, and visible effort rather than actual output.

As a result, workers who achieve dramatic productivity gains face a strategic dilemma: they can reveal their true productive capacity and demonstrate that they are capable of completing ten hours of work in one, or they can maintain a conventional performance profile while privately retaining the surplus time created through technological leverage.

The first strategy often produces a predictable outcome. Organizations respond to exceptional productivity by raising expectations. Higher output becomes the new baseline. Additional responsibilities are assigned. Performance targets increase. In many cases, compensation remains largely unchanged. The end result is that the worker has effectively converted technological leverage into additional obligations.

The second strategy treats productivity gains as a private asset. Corporate objectives are met. Deliverables are completed on time. Performance expectations are satisfied. But the hours reclaimed through automation are redirected toward activities that generate independent value: building products, acquiring customers, developing intellectual property, or launching new ventures. From the worker’s perspective, AI-generated productivity gains become a form of retained economic surplus rather than a subsidy transferred back to the employer.

This raises immediate legal and ethical questions.

Indeed, almost all corporate employment contracts contain explicit “conflict of interest” or “exclusivity of service” provisions that prohibit moonlighting, along with a common law “duty of loyalty” that mandates the employee act strictly in the employer’s financial interest during working hours: under statutory and common law, utilizing an employer’s equipment, resources, or leased time to build a private venture constitutes a breach of this duty. If discovered, the employer has the clear legal right to terminate the employee for cause, seek injunctive relief, claw back the salary paid during the period of disloyalty, and claim ownership of any intellectual property generated using company systems.

However, the defining difference between who grows in the modern economy and who remains stagnant is a sophisticated, realistic understanding of the relationship between legal text and compliance: any law, contract provision, or corporate policy that is not actively and systematically enforced, is practically non-existent. Enforcement requires monitoring, monitoring requires evidence, evidence requires resources.

As a result, the practical risk associated with productivity arbitrage depends less on the existence of contractual restrictions and more on the likelihood of detection and the severity of any resulting consequences. However, remote work has significantly altered this equation. Employers can monitor activity, track software usage, collect productivity metrics, and deploy increasingly sophisticated surveillance systems; yet these tools are often designed to identify underperformance rather than concealed efficiency. When an employee consistently delivers high-quality work on time, the incentive to investigate how that work was produced remains relatively low.

If an individual ensures that all assigned corporate deliverables are completed flawlessly and ahead of schedule, the employer has no immediate performance-based indicators or financial justification to initiate invasive audits or legal action. After all, the corporation’s core interest has already been satisfied: it received the output it contracted for at the agreed-upon price. The fact that the employee generated that output in a fraction of the required time through private technological leverage represents an arbitrage gain that belongs entirely to the worker, not the firm. And provided the worker maintains strict operational hygiene, the probability of detecting the productivity arbitrage approaches zero.

There is, however, a critical cognitive caveat that must be addressed: the risk of stunting professional judgment.

Traditionally, professional judgment, meaning the capacity to act wisely when formal rules are insufficient, is forged through the development of five core capabilities:

- evaluative;

- contextual;

- trade-off;

- anticipatory; and

- ownership judgment.

These capabilities emerge through sustained repetition, personal accountability, and direct engagement with imperfect, ambiguous, and often messy work. If early-career analysts merely review AI-generated outputs rather than producing them independently, they risk failing to develop the pattern recognition, intuition, and professional skepticism necessary for sound decision-making. Over time, this could weaken the pipeline of professionals capable of exercising independent judgment under conditions of uncertainty.

The solopreneurial model, however, offers a solution to this developmental bottleneck. A rational worker does not use AI to avoid cognitive effort and drift into passivity; rather, they redeploy the cognitive capacity liberated by automation away from low-leverage corporate bureaucracy and toward the high-stakes, real-world execution of their own ventures. Operating a private business demands the rapid development of all five forms of professional judgment at a pace and intensity that few corporate training programs can match: the individual learns to allocate capital, design products, acquire customers, and navigate legal and operational constraints, cultivating genuine cognitive sovereignty while benefiting from the financial stability provided by salaried employment.

VI: The Solopreneur’s Playbook

The ultimate objective of the Sovereign Builder is to construct an economic asset that is resilient, scalable, and capable of generating value independent of the builder’s direct work. Ideally, high-margin and digital-based too, to give them location freedom other than time and financial freedom.

According to demographic entrepreneurship surveys, the primary obstacle cited by 44% of aspiring side-hustlers is time management, the lack of hours in the day to manage a full-time corporate role while simultaneously building a private business. To overcome this constraint, the modern builder must systematically integrate AI and automation tools to streamline, automate, and delegate repetitive operational tasks. Rather than acting as a manual laborer in their own business, they must act as a systems architect, utilizing software to build a “digital estate” that operates continuously, asynchronous to their physical time.

The core strategic framework for this digital estate is a concept known as Building in Public, the deliberate act of documenting the development of a venture in real time. Founders openly share progress, decisions, experiments, lessons, failures, and milestones with an audience through social media, newsletters, podcasts, and other digital channels. At its core, building in public functions as a distribution mechanism: by continuously documenting the process of creation, founders generate attention, attract feedback, establish credibility, and create opportunities for collaboration long before a product reaches maturity. Rather than treating audience development as a separate activity, distribution becomes embedded directly into the act of building.

| Strategic Dimension | Traditional Corporate GTM Model | Build-in-Public Model |

|---|---|---|

| Marketing Approach | Institutional branding and paid acquisition | Ongoing documentation and personal narrative |

| Feedback Cycle | Periodic market research and structured testing | Continuous audience feedback and rapid iteration |

| Trust Formation | Reputation derived from organizational credibility | Reputation derived from visible execution |

| Distribution | Advertising budgets and formal sales channels | Audience-driven distribution and community growth |

| Asset Ownership | Controlled by the organization | Controlled by the builder |

Building in public operates across three distinct layers of content creation, systematically converting transparency into accumulated trust and economic leverage:

-

The first layer consists of observable results: product launches, customer milestones, revenue growth, usage statistics, and major achievements provide evidence that progress is occurring. Unlike traditional corporate communications, which typically reveal only polished successes, the build-in-public model emphasizes ongoing transparency. The objective is not self-promotion but credibility. Demonstrated outcomes create trust more effectively than abstract claims.

-

The second layer focuses on the knowledge generated during execution: founders share technical discoveries, operational mistakes, marketing experiments, product decisions, and unexpected insights encountered along the way. By documenting what worked, what failed, and why, they transform personal experience into public value. This creates a mutually reinforcing relationship between builder and audience. The founder gains visibility and trust, while the audience gains practical knowledge.

-

The third layer exposes the decision-making process itself, and invites the audience directly into the decision-making process in real time. By posting open-ended questions about product features, seeking feedback on UI/UX mockups, or discussing contrarian industry perspectives, the builder transforms the customer from a passive consumer into an active participant in the venture’s creation.

To sustain this process over long periods, builders require a repeatable communication framework. One practical approach is the Rule of Thirds:

-

One-third of communication focuses on progress: product launches, customer outcomes, growth milestones, and visible achievements.

-

One-third focuses on challenges: technical failures, setbacks, incorrect assumptions, operational mistakes, and lessons learned through adversity.

-

One-third focuses on value creation: educational resources, templates, tutorials, tools, and practical insights that can be immediately applied by others.

This balance prevents communication from becoming either self-promotional or purely educational: progress demonstrates momentum, struggles establish authenticity, and resources create utility. Together, these elements compound into a durable distribution asset.

While traditional venture-backed startups burn millions of dollars in paid advertisement channels to acquire customers, the solopreneur utilizes their documented journey to build an organic distribution loop with a CAC of basically zero. The audience becomes a self-sustaining marketing force, actively sharing the product, writing reviews, and defending the builder against competitors because they are psychologically invested in the builder’s personal success.

Over time, the documented journey becomes an asset in its own right. The audience, reputation, archives, relationships, and accumulated trust generated through years of visible execution form a distribution network that can be carried from one project to the next. And unlike a paid advertising campaign, these assets continue to compound long after the original content has been published.

Liked it?

Subscribe to the newsletter to receive the next ones in your inbox as soon as they get published. It's free.